How so? Did Bush shove unwanted, un-applied for loans down the American publics throat? How is better qualified to tell what you can afford or not the govt. or yourself? Personally I do not want the govt. telling me what is what in my person affairs, apparently some of you need to be told how to live your lives.ATG wrote:

Yup.

The real problem in our economy is that Bush and his minions let big oil and big interest banks fuck us to the point of breaking.

What absurdity? Is it really so absurd to point out how us Americans bitch and complain about how tough our lives have become, yet seem to manage to come home with game consoles, IPOD's, cell phones, new PC's, the latest video cards and gaming accessories. The OP suggest that maybe a new perspective should be sought in America if we think our lives are so unlivable now because gas is "killing us" and we can not manage a budget anymore due to this "economic crisis". Yet we have the latest video games, and gaming machines and other gadgets by god!!DonFck wrote:

In an attempt to clean this thread up (you know who you are), I became astounded by its total and utter weirdness.

Be as it may, the people who can't see some of their posts any longer in this thread, I advise you to either post relevant and constructive material or to shut your traps, regardless of the absurdity that the OP suggests.

Cool?

IF they are buying them and can afford them to buy I agree, IF they are charging them, ( which I will be they are) then it is a problem.Bertster7 wrote:

Do you spend a large proportion of your income on frivolous rubbish?lowing wrote:

Yeah now there is a twist, I blame everyone for my problems except me.GorillaTicTacs wrote:

Expect lowing and his ilk to keep going further "off the reservation".

Its a solidified 12-point spread now, and only growing.

The wingnuts will get even more shrill in the coming week or two, blaming the problems of the world on everyone except themselves. Have a heart though, their world is coming to an end and their world view will need to catch up. Its a traumatic experience for some people to do it all at once. Check out the recent audience make-up of McCain's rallies, the hard-core nuts that show up are even scaring him.

Pal, I pay my bills and I have never not once without exception taken any welfare from any taxpayers.

If not, you're not supporting the economy properly - like all those people out buying Wiis, who are doing their bit and driving the economy forwards.

Like I said, it is not the WII specifically, it is a priority issue and people may loose their homes but they will have the latest game machine IPOD camera phone or whatever other gadget is out their.IG-Calibre wrote:

Lowing has come out with some doozies it has to be said, but dismissing the current global economic catastrophe as "a conspiracy theory" based on sales of the wii has to be his best yet.

Yeah sure, a $500 console and a few $50 games brought the world to its knees.

A $500,000 mortgage might have been the clincher.

Americans live well beyond their means as a nation, printing $700bn and sending it to China isn't going to help.

A $500,000 mortgage might have been the clincher.

Americans live well beyond their means as a nation, printing $700bn and sending it to China isn't going to help.

Last edited by Dilbert_X (2008-10-11 23:15:04)

Everything is great

/facepalmlowing wrote:

If there is any fraud it is from people who applied for loans they knew they could not afford or have any intention of repaying, I would even call it theft.Pierre wrote:

Bottomline: the mean reason is the greed of the bankers: they activily sold loans to people who they knew would never be able to repay, and next they covered these loans up and resold them (credit swaps) worldwide so they wouldn't get stuck with them when the ball would drop.

Maybe you would call that 'personnal responsability'. I'd call it fraud.

Is it nice living in your black and white world, where you can disregard all circumstances that you don't like or (most of the time) you don't understand?

Dream on, Lowing, keep making a lot of noise, because that's what it is, just noise.

As I illustrated in my picture (which sadly got deleted ) the 'lowing' set and the 'reality' set do not intersect.Pierre wrote:

/facepalmlowing wrote:

If there is any fraud it is from people who applied for loans they knew they could not afford or have any intention of repaying, I would even call it theft.Pierre wrote:

Bottomline: the mean reason is the greed of the bankers: they activily sold loans to people who they knew would never be able to repay, and next they covered these loans up and resold them (credit swaps) worldwide so they wouldn't get stuck with them when the ball would drop.

Maybe you would call that 'personnal responsability'. I'd call it fraud.

Is it nice living in your black and white world, where you can disregard all circumstances that you don't like or (most of the time) you don't understand?

Dream on, Lowing, keep making a lot of noise, because that's what it is, just noise.

So, the current economic state is entirely to do with people buying games consoles. It has nothing whatsoever to people being handed mortages they can't repay like I get handed leaflets when I go into town, or banks spending money like it grows on trees.

Ok lowing.

Ok lowing.

#rekt

No, lowing believes the lenders had nothing at all to do with the problem, that the businesses that bought up the loans from the banks had nothing to do with causing the problems either, and that it all comes down to people buying luxury items such as the Wii instead of paying off mortgages.

"Americans live well beyond their means as a nation"Dilbert_X wrote:

Yeah sure, a $500 console and a few $50 games brought the world to its knees.

A $500,000 mortgage might have been the clincher.

Americans live well beyond their means as a nation, printing $700bn and sending it to China isn't going to help.

Now yer getting it, it isn't just gaming machines ( I used it as an example of American gluttony) we charge and are making payments on fucking shoes.

and to think, with all of your superior knowledge about the world around you, all the consumer had to do was, NOT buy a home they couldn't afford, and/or refuse to pay artifically inflated house prices. I am guilty of the the later, however, I can afford my mortgage, I have excellent credit in the first place and did not need or want some bullshit sub-prime loan. The responsibility is on the consumer tp know what he can afford or should afford. The market will always reflect that attitude.topal63 wrote:

You are insane if not ignorantly insane. I just made that affliction up - and yet you're a suffering from it. How is that possible?lowing wrote:

If there is any fraud it is from people who applied for loans they knew they could not afford or have any intention of repaying, I would even call it theft.

You're like 47 right? Like about a 2-years or so older than me right? I would assume that gave you at least 2 years more on planet earth to actually know something right? Or at least have a minor interest in knowing what is actually going on within the country you live in. Forget it I am sticking with my original prognosis - you're ignorantly insane.

Mortgage brokers committed all kinds of fraud. In Florida (here in good old Disneyland, paradise, etc) they found-out (Gov. Crist studied the problem and concluded what everyone already knew) that there was virtually no regulation governing those who obtained broker licenses. Actual convicted criminals were allowed to obtain licenses. Sometimes the loan-default rates were 40% without a person ever making a single payment ever. Not one mortgage payment. Does that compute in your brain? Or does that have to spelled out to you what it means - it means there may have never been a buyer = total fraud. Another scheme has non-Americans (not illegals; foreign criminals) obtaining loans at 125% of the value and thence repeating - bilking the system with easily-obtained no-money-down fraud-value loans multiple times. Then skipping the country with the 25% difference. About 50% of the housing bubble was caused by speculators and investors alone (not people wishing to obtain a first-time homestead). About 25% of the bubble was developers following the market and getting away with insane new-home price increases. That is a definition of the bubble; which is in fact a PRICE POINT. The remaining 20%-25% valuations are normal, yet high, for home price increases in such a time period. The purely-fraudulent percentage is actually an unknown (with brokers). But make no mistake while there is some blame to lay rest at the hands of those who could nor afford it - that blame is minimal and its influence minimal.

http://www.sun-sentinel.com/business/sf … 9485.storyhttp://thehousingbubbleblog.com/index.htmlSince September 2007, federal prosecutors have charged 112 individuals for frauds involving loans worth more than $176 million, U.S. Attorney R. Alexander Acosta said.

According to industry groups, Florida leads the nation in mortgage fraud, accounting for nearly one quarter of all fraudulent loans.

One recent federal prosecution involved the purchase of 79 properties in Miami-Dade and Broward counties between 2005 and 2007 for roughly $24 million. The fraudulent activity ultimately resulted in several foreclosures and cost lenders more than $5 million, prosecutors allege.Those pushing the paper/sold mortgages to speculators and investors multiple times DRIVING the price UP; like a commodity. With 300% increases in a 5 year period not being uncommon. THE BIGGEST REASON WHY THERE IS A HOUSING BUBBLE HAS VIRTUALLY EVERYTHING TO DO WITH THE ARTIFICIALLY INFLATED HOME-PRICES. And those at the top - made money while all this bullshit was going on. They resold the paper - passing the risk. They insured the risk passing that on as paper sold as a derivative. All the while the financial-middlemen who does not contribute to society but rather leeches off it - made HUGE returns in the short term for WALL-STREET. Your politicians - nearly everyone knew what was going on (Rep & Dem alike) and did nothing about. If you think it wasn't knowledge; or known; until a graph was published in 2005 indicating the housing bubble - you are wrong. It was known. And for 2 and half more years not only did they let it continue happening - but some of the worst loans were given at the highest market-valuations - and the most amount of (even broker driven) fraud was committed. And the derivative market was ballooning as well - on a street no where near MAIN STREET USA.“A ‘cash back‘ mortgage swindle involving in excess of $1 million in stolen funds and more than $11.3 million in fraudulently obtained loans on 16 homes in the Sacramento region was alleged Friday in a federal indictment. ‘Over the course of numerous investigations we have seen how fraud-for-profit mortgage schemes took root in our Sacramento-area housing market, particularly in the 2005 to 2006 time frame of this case,’ said U.S. Attorney McGregor Scott.”

http://www.safehaven.com/article-3639.htmI mean honestly lowing you are know-nothing blow-hard. I have (engineering development projects where) single-family subdivisions that were; 60% unoccupied at one point (investors; not home-buyers). 80% vacancy rates in Condominiums. A single investor bought 2/3 of an entire town-home subdivision.These days, "Get Rich Quick" has been the mantra for too many people trying to cash in while buying real estate speculatively. With so much "free" money still flowing from the Federal Reserve, it has become a real estate speculator's dream world. These so called speculators have purchased over 3 million residences, practically with their eyes closed, with the sole intention of flipping them like pancakes to the next guy, marked up 25 percent or more. However, signs are beginning to appear that indicate this game of getting rich quick may soon be over.

Less than 20 percent of Californians can now afford a home with a fixed rate mortgage. The Federal Reserve is still raising variable interest rates. In 2004, when the housing bubble was really gathering steam, the National Association of Realtors calculated that 23 percent of homes purchased were for investment, and 13 percent were for second homes. With housing prices in some markets rising 20 to 40 percent in the past year - and 50 to 100 percent or more since 2000 - buying a house on spec looked like a sure thing to make a quick profit. But this housing deck of cards, in an already over-heated market, could have a domino affect. Why?

Home sales run about 9 million a year (this includes housing starts of 2 million and existing home sales of 7 million). If over 20 percent of homes purchased are investor properties, it appears that practically all new housing starts in America are accounted for by speculative buying. If second home buyers are added into the equation, speculative and investment buying of real estate (not owning to live in) actually exceeds total housing starts!

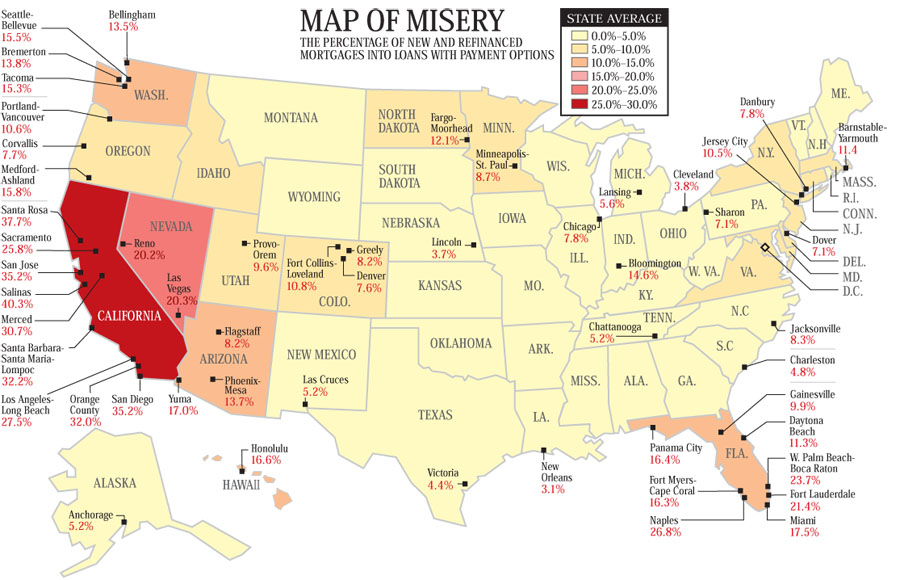

http://seattlebubble.com/blog/wp-conten … isery0.jpg

Also the concentrations of the bubble are isolated to specific markets heavily influenced by market speculation (get rich; easy money schemes and scheming). And, then dragging the whole economy into the problem - even though they (other areas) didn't enjoy the same market-valuations; steep home price increases.

Foreclosures:

http://creativeclass.typepad.com/thecre … sures.jpeg

Not subprime foreclosures:

http://bigpicture.typepad.com/comments/ … bntown.gif

You think your neighbor is to blame because his priorities weren't in order. You're right - excepting it wasn't your neighbor but something is out of order. The Gov., the Federal Reserve, Wall-Street, investors and speculators wanting to get rich quick without doing work - do not have their priorities in order. They want it all without having to get a blister on one little finger (power and money; or money thence power; whatever). They want it all - and they really don't want the risk either. So now that very same group is passing the risk and losses associated with risk onto taxpayers and future taxpayers; or rather they are trying to pass the associated risk.

{kind=link}

{kind=link}

{kind=link}

Actually, if you read the thread, I used the WII as ONE example as to American attitude and priorites in regard to finances. Sorry ya missed that point.Mint Sauce wrote:

So, the current economic state is entirely to do with people buying games consoles. It has nothing whatsoever to people being handed mortages they can't repay like I get handed leaflets when I go into town, or banks spending money like it grows on trees.

Ok lowing.

There's two parts to the equation. You are correct, but so is lowing. You can choose who to blame. I blame the consumer...why?topal63 wrote:

Are you dense... how is speculator, investor or someone (sometimes even a convicted criminal given a mortgage broker license) looking to get rich and make money by treating a homestead like a commodity - anything like a consumer? Or did reality just pass you by again.

What's the risk for someone who put NO money down and lives in a house they can't afford? They lose the house they can't afford, their credit rating is screwed. And now, in most states, if you claim your house under the homestead exemption you can't lose your house if you file for bankruptcy. So you got a house you can't afford, and now no one can force you to move. Oh, the humanity!

But unfortunately, those who took the gamble now are going to be strapping those who do own houses with an increase in property tax, and a long period of watching their house values fall. But remember, the demand for housing in some areas drove up the prices, partly by allowing those who wanted a riskless mansion to get a mortgage. So this is a market correction.

Sure, lack of regulation was an issue, but ultimately living beyond your means is the cause.

gee, I can't wait til Obama is elected President.

Lowing, it's like iPod and Wii.

Not: IPOD and WII

just to help you out mate!

Not: IPOD and WII

just to help you out mate!

Small hourglass island

Always raining and foggy

Use an umbrella

Always raining and foggy

Use an umbrella

Well then why is all the help of $700bn and upward going to the banks and corporations? They are both the blame, but only one area is going to be getting bailed out. Rightly or wrongly.Pug wrote:

Sure, lack of regulation was an issue, but ultimately living beyond your means is the cause.

Congress passed and Bush signed a law to give tax breaks for homeowners and to help with mortgage problems before the $700B, if you remember.TheAussieReaper wrote:

Well then why is all the help of $700bn and upward going to the banks and corporations? They are both the blame, but only one area is going to be getting bailed out. Rightly or wrongly.Pug wrote:

Sure, lack of regulation was an issue, but ultimately living beyond your means is the cause.

You said it yourself though,Pug wrote:

Congress passed and Bush signed a law to give tax breaks for homeowners and to help with mortgage problems before the $700B, if you remember.

Who's getting the rough end of the stick out of all of this? The average tax payer who didn't do anything wrong.Pug wrote:

But unfortunately, those who took the gamble now are going to be strapping those who do own houses with an increase in property tax, and a long period of watching their house values fall.

True, but the tax breaks cover the average taxpayer too. I never said it was enough though, but it's wrong to think nothing was done.TheAussieReaper wrote:

You said it yourself though,Pug wrote:

Congress passed and Bush signed a law to give tax breaks for homeowners and to help with mortgage problems before the $700B, if you remember.Who's getting the rough end of the stick out of all of this? The average tax payer who didn't do anything wrong.Pug wrote:

But unfortunately, those who took the gamble now are going to be strapping those who do own houses with an increase in property tax, and a long period of watching their house values fall.

That's exactly right. The tax breaks do nothing at all in comparison to the $700bn of tax payers money that could have gone elsewhere though.

With one hand they giveth a little, another they taketh alot.

With one hand they giveth a little, another they taketh alot.

Basic tenant of marketing - if there is no demand, there's no product.topal63 wrote:

Almost all of the price bubble was created by speculators and investors. Those paper contracts between NON-CONSUMERS and BANKS - equaled quick money. A majority of what went bust - was pure speculative money. The problem is the market could have weathered a lower PRICE POINT increase; it could not weather the paper losses of 30-50%. In the effective markets the speculator driven increases could not be held when they LET THEIR INVESTMENT PROPERTIES go bust.

I'm saying the demand for a no-risk loan and lack of regulation is ultimately because millions of people wanted easy way to own a home...and it was granted. Investors were only happy to oblige.

God forbid consumers take the responsibility for what they signed...I mean, with interest rates the lowest they have ever been...the absurdity of thinking the interest rate will not go up when you sign is ridiculous.

So we, as five year olds, beg for these high-risk mortgage loans...and when it bites us, we, as five year olds, whine it wasn't caused by us.

Ultimately, the government gave the consumer what they wanted.

Hold the phone...the ones holding aren't consumers?topal63 wrote:

I have investors/clients that have the capital to NOT LET THEIR properties go bust. They didn't - but others did. The ones holding aren't consumers and the ones the let the banks absorb the losses aren't consumers either.

You mean the ones holding the variable interest rate mortgages aren't consumers of the bank?

Sure, if you edit your post after I respond to it.topal63 wrote:

Pedantic misread.

You said market frenzy...what did your neighbor do before he was unemployed?

Ahh fuck it, you're reediting your posts...this is the third thread I've seen it after I'm done. Have a nice day.

Last edited by Pug (2008-10-12 08:36:59)

Well, how about including ALL the information in your first post then? Like explaining the difference between what consumer group you're talking about and WHY it makes a difference. Perhaps if that was there, there would be a few less posts.topal63 wrote:

Ahh fuck it... goddamn forum and an edit button... fuck that shouldn't be there; and crap I shouldn't explain what I meant when you misunderstand me; or in manner you're disagreeable with.

Anyways:

http://www.newsweek.com/id/162789"Second, many of the biggest flameouts in real estate have had nothing to do with subprime lending. WCI Communities, builder of highly amenitized condos in Florida (no subprime purchasers welcome there), filed for bankruptcy in August. Very few of the tens of thousands of now-surplus condominiums in Miami were conceived to be marketed to subprime borrowers, or minorities—unless you count rich Venezuelans and Colombians as minorities. The multi-year plague that has been documented in brilliant detail at IrvineHousingBlog is playing out in one of the least subprime housing markets in the nation."

WHAT DID YOUR NEIGHBOR DO?